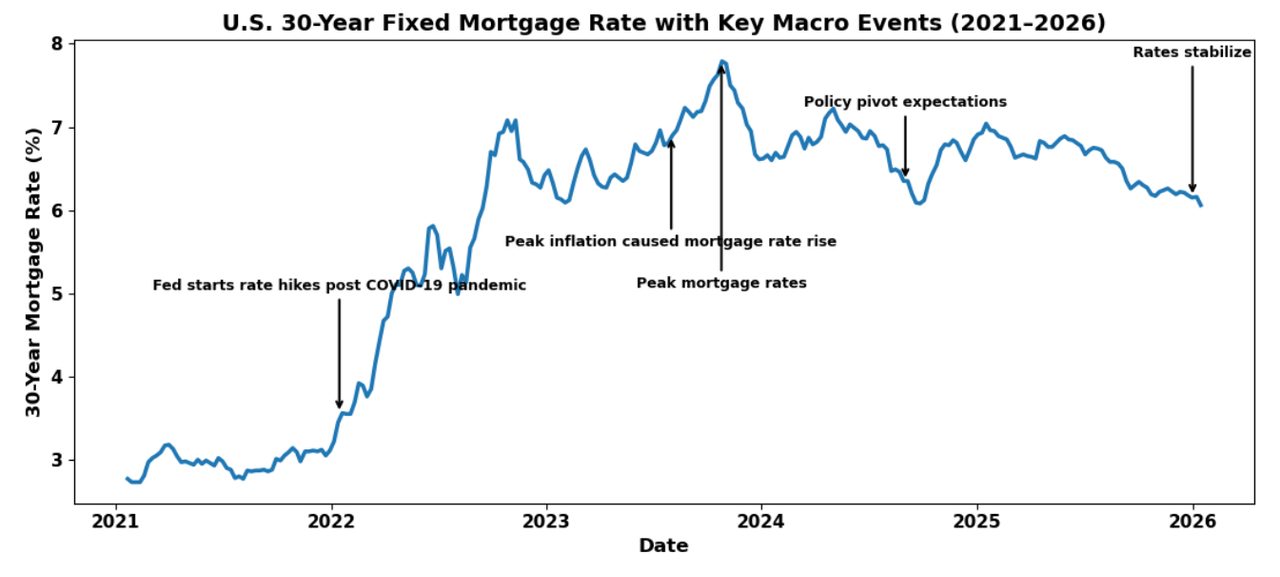

The thirty-year fixed mortgage rates in United States of America surged after the Federal Reserve began aggressive rate hikes in 2022, peaking near 7% in late 2023 before easing slightly in between 2024 to 2025 and now on January 15, 2026 30-Yr FRM 6.06% . Despite this moderation, borrowing costs remain well above pre pandemic levels, signalling a shift to a structurally higher rate environment. This marks a clear departure from the very low rates that drove post COVID housing demand, with tighter financial conditions continuing to constrain affordability and real estate activity.

Household Stress Signals

The second chart highlights how higher rates and elevated prices have translated into ongoing household financial strain. According to recent survey data, 19% of renters report falling behind on rent, 17% of adults did not pay all bills in full, and 65% say higher prices worsened their financial situation in 2023. These indicators suggest that the adjustment to higher interest rates is not merely a market-level phenomenon but one that continues to affect household balance sheets. Importantly, this stress persists even as inflation cools. This underscores the affordability challenges created during the tightening phase.

Office Space in the United States

The U.S. office market continues to adjust to a post-pandemic reality shaped by hybrid and remote work. Recent government and academic research confirms that this shift is structural rather than temporary. Data from the Bureau of Labor Statistics’ American Time Use Survey (ATUS) shows that remote work remains significantly above pre-2020 levels, with a persistent share of employed adults working from home on an average workday. Complementing this, Kastle’s badge-swipe data shows weekly average office attendance at 56.3%, while Placer.ai’s foot-traffic index shows Dec 2025 visits 33.1% below 2019 (or 36.2% on a working-day basis).

And

Census Bureau American Community Survey (ACS) data indicates that commuting patterns have not fully reverted, particularly in large metropolitan areas, implying sustained lower daily office utilization.

Transportation indicators from the U.S. Bureau of Transportation Statistics (BTS) reinforce this trend. Public transit ridership and weekday commuter travel volumes remain below pre-pandemic benchmarks, especially in central business districts, suggesting fewer workers are traveling to offices for their job. These mobility metrics provide an indirect but reliable signal of office attendance levels across major cities. Academic research published by the National Bureau of Economic Research (NBER) further documents the persistence of hybrid work models, noting that firms have increasingly optimized around flexibility rather than expecting a full return to office. Several NBER studies highlight that office demand has structurally declined in sectors with high digital task content, contributing to higher vacancy rates and weaker rental growth.

From a financial stability perspective, the Federal Reserve’s Financial Stability Report (November 2025) notes that while commercial real estate prices particularly office properties have shown signs of stabilization after sharp declines, vacancy rates remain elevated and refinancing risks persist. The report emphasizes that lower office utilization has constrained income growth for landlords and increased pressure on valuations, especially for properties acquired during the lower interest rate era.

Source: , .

Bottomline

Taken together, the data point to a U.S. real estate market undergoing a prolonged structural realignment rather than a collapse. Elevated interest rates have reduced affordability and transaction activity, household stress remains elevated, and office demand has yet to return to pre-pandemic norms. Even as expectations of eventual policy easing emerge, the path forward is likely to be uneven. Outcomes across real estate will increasingly depend on asset quality, location, tenant mix, and balance sheet resilience. In a higher rate world, the adjustment process is ongoing and its effects will continue to shape both residential and commercial real estate in the years ahead.

This article is for informational purposes only and does not constitute investment advice.