By Anupriya Halder

Chinese Index Price to EarningsSnapshots: November 2025

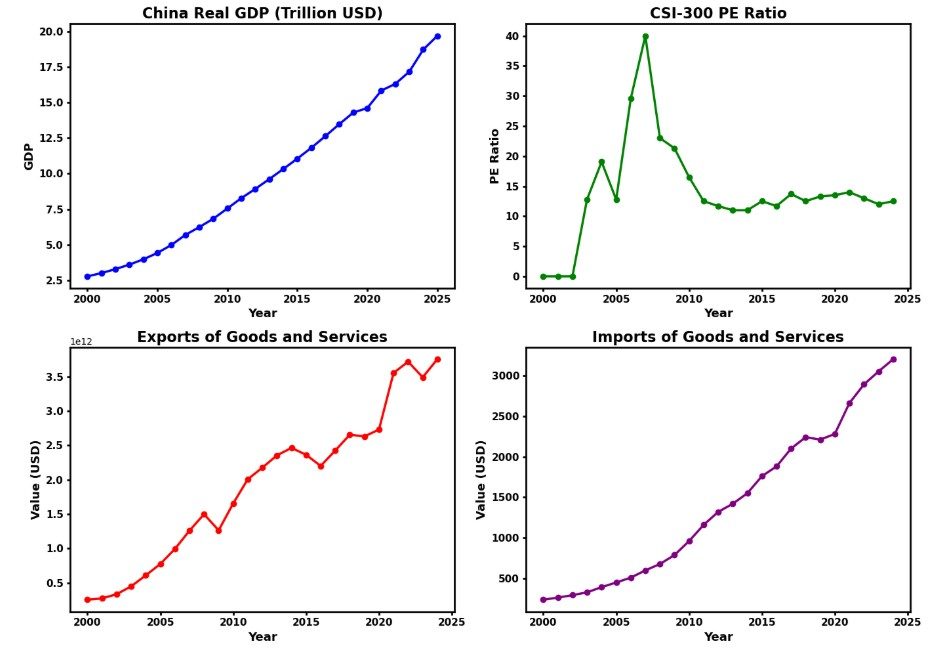

As of mid of November 2025, major Chinese equity indexes exhibit markedly different valuations. The CSI 300, a key barometer for China’s blue chips, stands at a P/E of 17.0, tracking a yearly gain of 16.6%. The Hang Seng Index (HK50) in Hong Kong trades at a P/E ratio of about 14.6, reflecting positive momentum with a year-to-date return of 36.8%. On the mainland, the Shanghai Composite Index is at a P/E of 16.4, having rallied nearly 20% over the past twelve months, while the large-cap Shanghai 50 index remains relatively modestly valued with a P/E ratio of 10.8. These metrics indicate stretched valuations versus historical averages, particularly for the CSI 300 and Shanghai Composite. However, the valuation premium for the HK50 and Shanghai 50 is still moderate on an absolute basis. The divergence in P/E ratios and price performance reflects robust foreign inflows into Hong Kong, ongoing recovery in domestic A-shares, and persistent sectoral rotation within China’s equity landscape.

Chinese Index Valuations Remain Discounted vs Global Benchmarks

Presently there is a stark valuation divergence between Chinese and global equities. The S&P 500, the leading US benchmark, currently trades at a P/E of 27.9 to 30.4, reflecting rich valuations amidst continued earnings growth and tech sector leadership. The Nikkei 225 in Japan stands around 19.2 to19.9, whereas the FTSE 100 in the UK stands at 19.1. This shows moderate valuations among developed markets. Compared to historic trends, most Chinese indexes are discounted against their global peers, driven by cautious sentiment over domestic macro fundamentals and regulatory risks. These figures highlight that Chinese equities especially large caps are currently present at a substantial valuation gap versus their international counterparts, suggesting there may be both downside protection and potential upside for value-oriented investors.

Top CSI 300 Stocks and Their Price to Earnings Ratios: Key Drivers of Index Valuation

This CSI 300 index’s current valuation is driven largely by its top ten constituents, which collectively form about 22% of the index’s market capitalization. Leading the pack is Kweichow Moutai, the premium liquor maker, with a significant 4.6% weighting and a P/E ratio of 29.7, reflecting strong brand pricing power. Contemporary Amperex Technology (CATL), a major EV battery producer with a 3.4% stake, trades at a P/E of 26.1. Financial players such as Ping An Insurance and China Merchants Bank contribute notable weightings of 2.7% and 2.3%, with relatively low P/E ratios of 7.7 and 8.1, respectively, underscoring more conservative valuations. Other key names like Midea Group (P/E 12.4), China Yangtze Power (P/E 17.2), and brokerage firm CITIC Securities (P/E 10.2) display mid-range multiples. East Money Information, a financial data firm with P/E 36.3, and Industrial Bank, valued at P/E 5.7, highlight the broad spectrum across sectors in the index. These varying multiples collectively drive the CSI 300’s moderate overall valuation, offering insight into sector specific investor sentiment and growth expectations within China’s equity market.

Navigating Involution, Deflation, and Structural Reform in China’s 2025 Economy

China’s economy now is grappling with the intertwined challenges of involution, deflation, and structural reform, as extensively analysed in the China Leadership Monitor (Sep 2025). Real GDP growth was 5.2% year-on-year in Q2 2025, but nominal growth slowed to 3.9%. This is less than half the Covid-19 phase. Persistent deflationary pressure is evident, with producer prices falling since mid of 2022 and consumer inflation averaging only 0.2%, far below the global average. The historic property sector collapse has shifted the economic growth engine toward services, now contributing 80% of growth since 2023. Beijing’s structural reform efforts focus on combating “involution,” a destructive price competition eroding profits by 30% from 2021 to June 2025, while losses increased from 14% in 2019 to 27%. This anti-involution campaign targets excess capacity and margin erosion, particularly in emerging sectors like EVs and solar panels. Despite external headwinds from U.S. tariffs and trade tensions, China sustains export growth through market diversification and export controls. Fiscal stimulus and cautious monetary easing underpin these reforms, while Beijing patiently prioritizes long term self-sufficiency and technological industrial leadership over short term growth stimulants. This strategic stance aims to recalibrate China’s economic model amid complex external pressures and internal imbalances.

Bottom line

China’s equity markets currently seem to be at a significant valuation discounts compared to major global peers like the S&P 500, Nikkei 225, and FTSE 100. These discounts reflect ongoing macroeconomic challenges including deflation, a property sector collapse, and a structural shift from investment driven to consumption and tech driven growth. Beijing’s active campaign against “involution” aims to reduce destructive competition and improve industrial profitability. There may be chances of a structural reform agenda focused on sustainable long-term expansion. This environment may be offering a compelling opportunity to invest. There are fiscal stimulus, cautious monetary easing, and policies encouraging shareholder returns. However, an investor should always stay alert to geopolitical risks and domestic reforms’ pace. Overall, China seems to be offering both value and growth prospects amid a complex but strategically guided economic transformation.

Disclaimer: The source of the data is , .

This article is for informational purposes only and does not constitute investment advice.